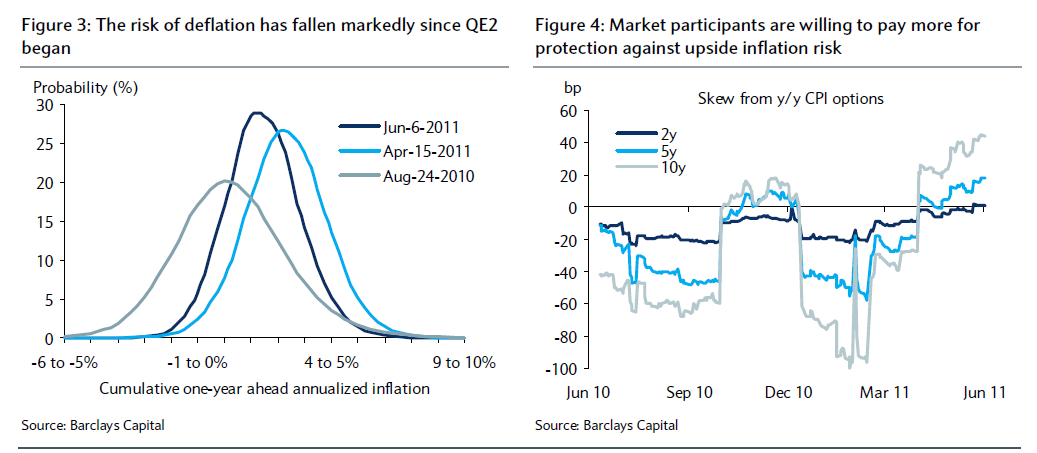

The increase in inflation and inflation expectations has also coincided with a reduction in deflation risk. Figure 3 shows the probability of cumulative inflation over a one-year horizon using information from both TIPS and CPI options data. The figure shows that the probability of deflation over the one-year ahead horizon in August of last year was 36%. When 5y5y breakeven inflation reached its recent high in April of this year, the probability had fallen to about 3%. Currently, it stands at about 7%. In addition, Figure 4 shows that the market remains more willing to pay for protection against upside inflation risks than protection against excessive deflation risk. The figure plots the difference in premiums paid on +200bp out-of-the-money inflation caps and -200bp out-of-the-money inflation floors for different horizons. Because an inflation cap pays off when cumulative inflation exceeds the threshold specified in the contract, a positive reading is an indication that the caps are more expensive than the floors; in other words, the market sees the distribution of expected inflation as skewed in the direction of upside inflation risk. The trends from CPI options markets suggest that skew has been moving in the direction of willingness to pay for protection against upside inflation risk, whereas for much of last year, participants were willing to pay more for protection against deflation.

Altogether, we see the trends in inflation markets as consistent with Chairman Bernanke’s comments in his April press conference that the balance of risks between seeking additional progress on its dual mandate relative to further balance sheet expansion was “less attractive” than it was a year earlier. We therefore see the Fed as inclined to remain patient. If incoming data confirm the Fed’s view that the economy is turning up in the second half of the year, the FOMC will likely continue on its path towards normalizing the policy stance. However, if the recovery fails to regain momentum, the balance of risks may shift back in favor of further Fed action.

Click on charts to enlarge, courtesy of Barclays Capital.

Well, just in case ... "if the recovery fails to regain momentum". Why it should?

No comments:

Post a Comment